Your mother passed away a few weeks ago. While you were still sorting through the paperwork on her kitchen table, a letter arrived from a mortgage servicer you'd never heard of, with phrases like "due and payable" and "loan balance" — and a number that made your stomach drop. You knew she had a reverse mortgage. You did not know that, now, it was somehow your problem, with what looked like a deadline attached.

Take a breath. This is solvable, and the most important thing to understand up front is this: you almost certainly do not owe this money out of your own pocket. A reverse mortgage in California is a non-recourse loan — the house is the collateral, not you. As an heir you have three real paths, the right one depends on whether there's equity left in the home, and you have more time than the first scary letter suggests. Here's exactly how it works.

The one thing most heirs get wrong: you don't "inherit the debt"

This is the reframe that changes everything, so read it twice. A reverse mortgage — almost always a HECM (Home Equity Conversion Mortgage), the FHA-insured kind — lets a homeowner 62+ pull equity out of their home as cash while they live in it. They make no monthly payments; instead the balance grows over time as interest and insurance accrue. When the last surviving borrower dies (or permanently moves out), the loan becomes "due and payable."

Here's the part that calms most people down: because a HECM is non-recourse, neither you nor the estate can ever owe more than the home is worth. If the loan balance is $480,000 and the house is worth $850,000, there's $370,000 of equity that belongs to the heirs. If the loan balance is $620,000 and the house is only worth $560,000, you are not on the hook for the $60,000 difference — FHA's insurance covers the shortfall. You don't write a check from your savings. The worst case is that you walk away with nothing; it is not that you walk away owing money.

So the real question is never "how do I pay off Mom's loan?" It's "is there equity in this house, and how do I capture it before the clock runs out?"

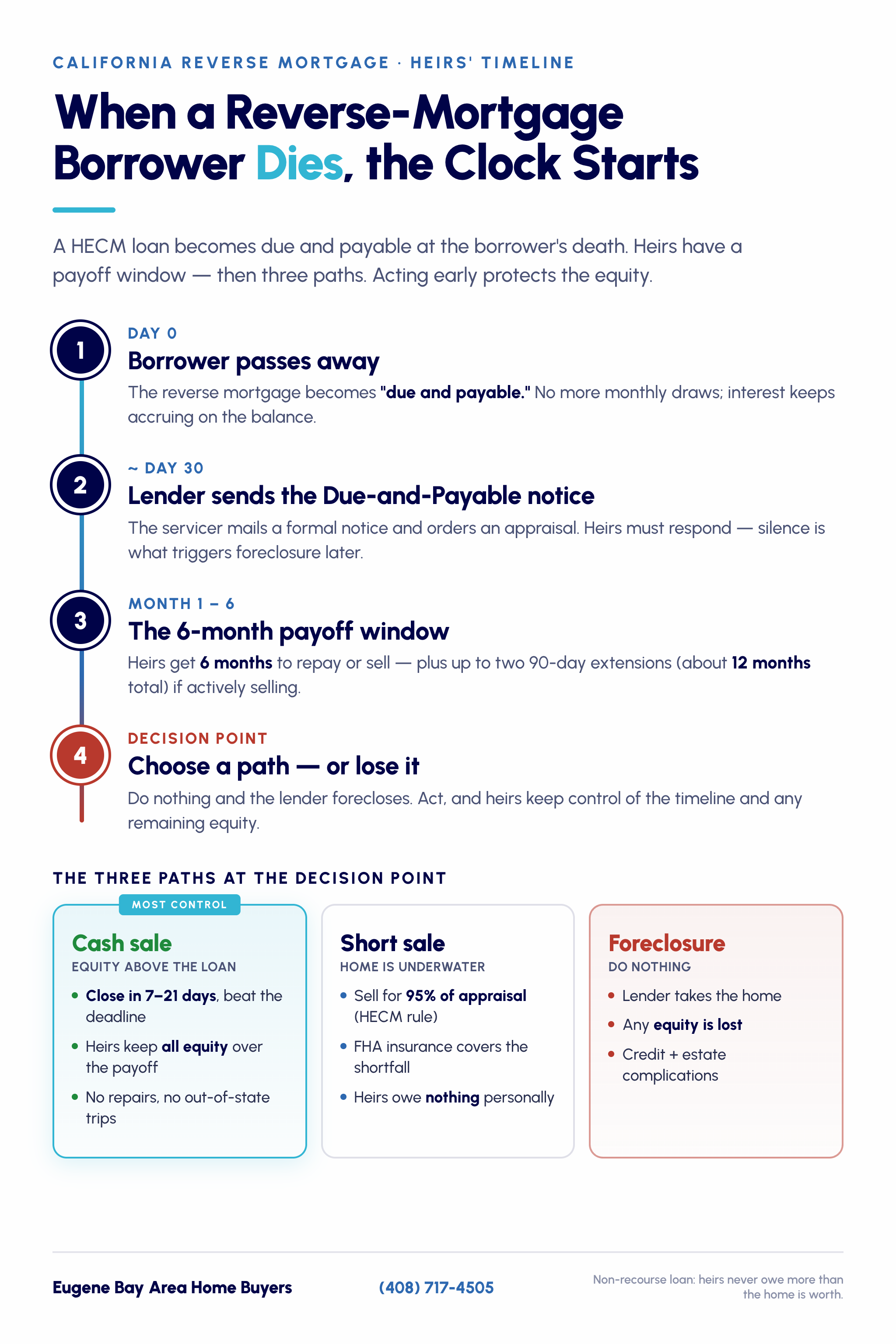

The timeline: what the "due and payable" clock actually looks like

The letter that scared you has a deadline buried in it, but it's not a guillotine. The HUD-regulated timeline for a HECM after the borrower's death generally runs like this:

- Day 0 — the borrower passes away. The loan becomes due and payable. No more draws come out; interest and the mortgage-insurance premium keep accruing on the existing balance, so the payoff number creeps up by roughly $2,500–$3,500 a month on a typical Bay Area balance.

- Around day 30 — the servicer sends a "Due and Payable" notice and orders an appraisal to establish current value. Heirs are generally expected to state their intent — sell, keep, or surrender — within about 30 days of this notice, even though the full payoff window runs from the date of death. This is the moment to respond: foreclosure later is almost always the result of heirs ignoring these letters, not of them missing an impossible deadline.

- Months 1–6 — the payoff window. Heirs generally get 6 months to repay the loan or sell the home. If you're actively marketing or selling the property and keeping the servicer updated, HUD allows up to two 90-day extensions — roughly 12 months total. You request these in writing; they are not automatic.

- The decision point. Do nothing and the lender forecloses, and any equity is lost to the foreclosure process. Act — repay, sell, or short-sell — and you stay in control of both the timeline and the money.

The figure below maps the whole sequence, including the three paths heirs choose between at the decision point.

Your three real options as an heir

Option 1: Keep the home — pay off (or refinance) the loan

If the property has sentimental value or you want it as a rental, you can keep it by satisfying the loan. To keep a HECM home, heirs can pay the lesser of the full loan balance or 95% of the current appraised value. That 95% rule matters when the loan is underwater — you can buy the family home for 95% of what it's worth even if the balance is higher. Most heirs satisfy this with a regular mortgage refinance in their own name or with cash. Timeline: 30–60 days to close a refinance. Catch: you need to qualify for the new loan, and the carrying clock keeps running while you do.

Option 2: Sell the home — keep the equity above the loan

This is what most heirs do, because most Bay Area homes carry far more value than the reverse-mortgage balance. You sell, the loan gets paid off from the proceeds at closing, and every dollar above the payoff belongs to the heirs. You can sell the traditional way (list on the MLS) or to a cash buyer — the difference is speed and certainty, which we break down in the math section below. Timeline: 7–21 days for a cash sale, 60–90+ days for an MLS listing. Catch: if the home is dated or needs work (many are, after years of an elderly owner living there), a traditional listing means repairs and cleanout first, on a clock.

Option 3: The home is underwater — do a HECM short sale or deed-in-lieu

If the balance is higher than the home's value, heirs sell to a third party at 95% of the appraised value, the FHA insurance covers the shortfall, and — because it's non-recourse — the heirs owe nothing and their credit is untouched. Alternatively, a deed-in-lieu simply hands the keys back. Either beats letting it foreclose, which damages the estate and can drag on. Timeline: 30–90 days. Catch: you'll coordinate with the servicer and HUD, which is more paperwork than a clean cash sale.

The one option that's never in your interest is the fourth, invisible one: doing nothing. Ignore the letters and the lender forecloses, the equity evaporates into fees and a distressed sale, and you've lost the very money the non-recourse rule was designed to protect. If you've already missed a deadline or a foreclosure has started, the same urgency-and-options logic in our guide to how to stop a foreclosure in California applies here too.

Real Bay Area math: an $850K Oakland home, MLS vs cash sale

This is a representative scenario, not a quote — your numbers move with the home, the neighborhood, and the loan balance. Say you've inherited your father's 1960s Oakland home. It appraises at $850,000. His reverse-mortgage balance at death was $480,000 and is growing about $3,000 a month. The house needs the things a longtime elderly owner's house usually needs: a cleanout, a dated kitchen and bath, a 20-year-old roof. Here's how the two sale paths net out — and why the "bigger" number isn't automatically the better one.

One of these numbers is an estimate with a 4-month deadline attached. The other is firm and clears in two weeks. On an inherited reverse-mortgage home, certainty and speed aren't a luxury — they're what keeps the payoff clock from turning your equity into a foreclosure.

Read it honestly: the MLS path nets about $19K more on paper — and if the home were already market-ready, you weren't out of state, and the probate timeline was clear, listing would be the right call. But that $256K is an estimate that needs four months, a cleanout, repairs you pay for up front, and a buyer whose financing won't fall through — all while interest accrues and the payoff deadline ticks. The cash number is locked, needs no repairs, and closes with months to spare. When the clock is the real constraint, the smaller certain number protects more equity than the bigger fragile one.

Want to see how a cash buyer arrives at that $720K as-is figure? It's not a lowball — it's a formula, and we lay it out in how much cash home buyers actually pay. Selling in current condition with no cleanout is the norm for inherited homes; here's our full guide to an as-is sale in California.

Special cases that complicate a reverse-mortgage home

The home has to go through probate first

If your parent's home passes by will (or with no estate plan at all), it goes through California probate before you can legally sell it — and probate routinely takes 9–18 months, which can blow past the HECM payoff window. The two clocks don't sync, and that tension catches many heirs off guard. The fix is usually to request the HUD extensions in writing and sell during probate with court confirmation. Our guide to selling a house in probate in California walks through the steps; if the home was held in a trust or with a transfer-on-death deed, you may be able to sell after death without probate entirely, which keeps you comfortably inside the payoff window.

There are multiple heirs and you don't all agree

One sibling wants to keep the house, another wants the cash, a third lives out of state and won't return calls. A reverse-mortgage payoff clock does not wait for family consensus, and that pressure can force a faster decision than a normal inheritance would. We cover the mechanics — buyouts, partition, getting everyone to sign — in selling an inherited house with multiple owners. A clean cash sale is often the peace-keeper here because it closes before the disagreement hardens into a standoff.

A non-borrowing spouse is still living in the home

If only one spouse was on the reverse mortgage and the other is still alive and living there, an Eligible Non-Borrowing Spouse may be able to defer repayment and remain in the home under HUD's rules — the loan does not automatically become due. This is one of the most important and most misunderstood protections in the program. Confirm the surviving spouse's status with the servicer before anyone talks about selling.

There's also a tax lien or other debt against the property

Reverse-mortgage homes sometimes carry a second issue — unpaid property taxes, a tax lien, or other liens that have to clear at closing. These get paid out of the sale proceeds in priority order, which reduces what reaches the heirs but doesn't stop the sale. A cash buyer who handles distressed titles regularly can close around these; many traditional buyers can't.

FAQ: reverse mortgages and selling, for California heirs

Do I have to pay my parent's reverse mortgage out of my own money?

No. A HECM is non-recourse, so neither you nor the estate can ever owe more than the home is worth. The loan is repaid from the home — by selling it, refinancing it, or surrendering it. Your personal assets and credit are not at risk for any shortfall; FHA insurance covers the gap if the home is worth less than the balance.

How long do I have to sell before foreclosure?

Generally 6 months from the borrower's death, with up to two 90-day extensions (about 12 months total) if you're actively selling and keeping the servicer informed. You must request the extensions in writing — they aren't automatic. The fastest way to be safe is to get the home under contract early; a cash sale that closes in two weeks removes the deadline pressure entirely.

What happens to the equity above the loan balance?

It belongs to the heirs. If the home sells for $850,000 and the payoff is $490,000, the roughly $360,000 of equity (minus selling costs) goes to the estate and then to you. The lender only takes what they're owed; they don't keep the upside.

What if the reverse mortgage is more than the house is worth?

Then you have an underwater HECM. Heirs can sell to a third party at 95% of the appraised value with FHA insurance covering the shortfall, or hand back the keys via deed-in-lieu. Either way you owe nothing personally and your credit is unaffected. The only bad outcome is ignoring it and letting it foreclose.

Can I sell the house while it's still in probate?

Yes — California allows a sale during probate, typically with court confirmation. Because probate can run longer than the HECM payoff window, selling during probate (and requesting the HUD extensions) is often exactly the right move. See our probate selling guide for the steps.

Will selling to a cash buyer get me less than listing?

Often a bit less on the raw sale price — but on an inherited reverse-mortgage home, the cash path frequently nets more in your pocket once you subtract the cleanout, repairs, agent commission, and four months of accruing interest a listing requires. And it removes the foreclosure-clock risk. We're honest about it: if the home is market-ready, you have time, and there's no family or probate complication, listing may net more. When there's a deadline or condition issue, cash usually wins.

The servicer keeps calling. What do I actually say?

Tell them you're the heir, that you intend to satisfy the loan by selling, and ask them to note the file and send you the payoff statement and the extension request form. That single call moves you from "ignoring it" (the only path that ends in foreclosure) to "handling it." Then line up your sale.

The honest summary

A reverse mortgage on an inherited California home feels like a trap and is actually a fairly forgiving, well-regulated process — as long as you don't ignore it. You don't owe the debt personally. There's almost always equity that belongs to you. And you have months, not days, to act.

If the home is in good shape, you have time, and the family agrees, list it and capture the top dollar. If it needs work, you're out of state, you're staring down the payoff deadline, or probate is dragging — a cash sale that closes in two weeks protects the equity the program was designed to give you — and because of the stepped-up basis, the capital gains tax on the inherited home is usually minimal. Here's exactly how we calculate a fair as-is offer, with no repair credits or surprises later.

Want a real number on an inherited home with a reverse mortgage — and a straight answer on whether selling to us even makes sense for your situation? Call (408) 717-4505, send us the address, or start on our inherited Bay Area house cash buyer page. It's free, there's no obligation, and we'll tell you honestly if listing would serve you better. We buy across the Bay Area including Oakland, San Jose, and Hayward, and we close on your timeline — before the clock runs out.